CUMPDGM Procedure |

Performs a Durbin's Cumulated Periodogram test for serial correlation. The test statistic is a Kolmogorov-Smirnov statistic.

@CUMPDGM( options ) series start end

Parameters

|

series |

series to test |

|

start, end |

range over which to run the test. By default, the range of series |

Options

[PRINT]/NOPRINT

[GRAPH]/NOGRAPH

Example

calendar(q) 1947:1

open data haversample.rat

data(format=rats) 1947:1 2006:4 gdp

*

log gdp

diff gdp / diffgdp

diff(center) diffgdp

@cumpdgm diffgdp

This tests the de-mean log difference of GDP for serial correlation. If the series were a drifting random walk, this would show an insignificant test.

Sample Output

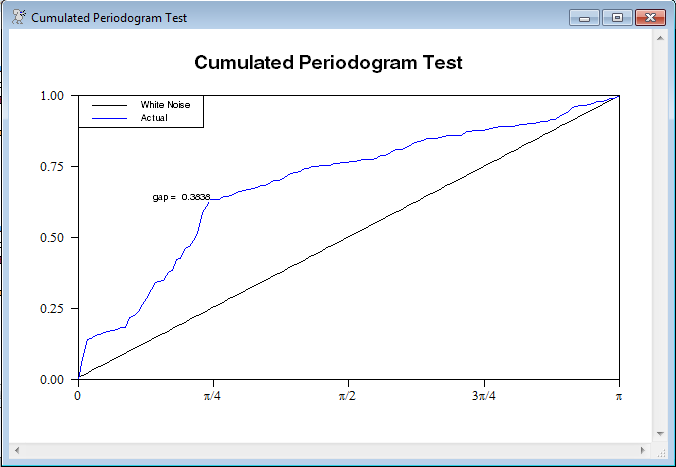

This is the output from the example above. The test statistic is well outside the rejection level. The graph shows a 45 degree line, which is where the blue line should be (roughly) if the series were white noise. Instead, it's fairly clear that the lower frequencies are more dominant than the higher ones.

Cumulated Periodogram Test for Series DIFFGDP

Maximum Gap 0.3838

At Frequency 0.7854

Approximate Rejection Limits

1% 0.1441

5% 0.1202

1% 0.1078

Copyright © 2026 Thomas A. Doan