ARMASPECTRUM Procedure |

@ARMASpectrum produces a graph of the spectral density for an input ARMA model where the model is in the form of an EQUATION. This could be an equation defined by BOXJENK or LINREG, or it could be a test equation created using EQUATION.

@ARMASpectrum( options ) eqn

Parameters

|

eqn |

EQUATION as source for spectral calculation |

Options

ORDS=# of frequency ordinates used [512]

HEADER=Header for graph

FOOTER=Footer for graph

Example

*

* Brockwell & Davis, Introduction to Time Series and Forecasting, 2nd ed.

* Example 4.1.5 from pp 119-122

*

* This uses the @ARMASpectrum procedure, which takes an input ARMA model

* and produces a graph of its spectral density.

*

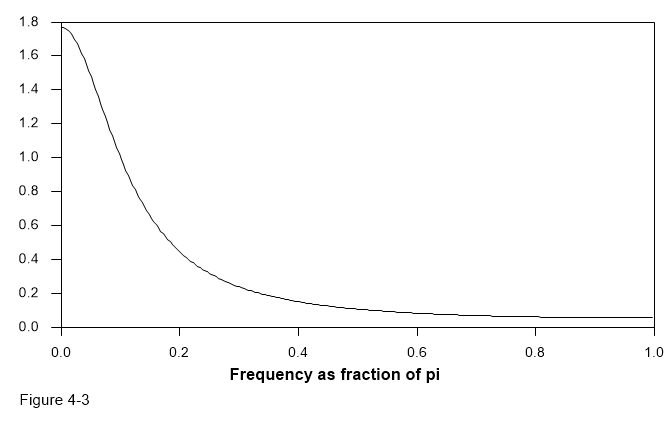

equation(noconst,coeffs=||.7||) ar1 y 1 0

@ARMASpectrum(footer="Figure 4-3") ar1

equation(noconst,coeffs=||-.7||) ar1 y 1 0

@ARMASpectrum(footer="Figure 4-4") ar1

equation(noconst,coeffs=||.9||) ma1 y 0 1

@ARMASpectrum(footer="Figure 4-5") ma1

equation(noconst,coeffs=||-.9||) ma1 y 0 1

@ARMASpectrum(footer="Figure 4-6") ma1

Graph (Sample)

This is from the first example (an AR1 with \(\rho=.7\)).

Copyright © 2026 Thomas A. Doan